Overview

Recent research for The Ripon Society shows that Republicans face a challenging environment at the beginning of 2018, but they still have important opportunities before them to make their case to voters as the midterms draw closer. The overall environment has improved for Republicans since the passage of the tax bill. The electorate is evenly split on supporting the plan since it has passed, and Republicans will have to make the case as to why and how voters will personally benefit from the plan. The Republican brand image remains a challenge, but as shown by the recent tax bill, the way to improve the brand is through offering products that address problems and personal concerns that voters have.

Personal outcomes are important, and the primary metric by which voters assess how well the economy is working, and will be the metric by which the electorate will evaluate the success of the tax bill. Specifically, cost of living and retirement are key concerns for the electorate, with health care being defined as the most challenging element of cost of living, and almost a third of voters expressing concern that their financial situation will not allow them to retire. In this environment, the electorate is engaged and looking for solutions from either party that will address the concerns that they face.

Most Important Personal Outcomes

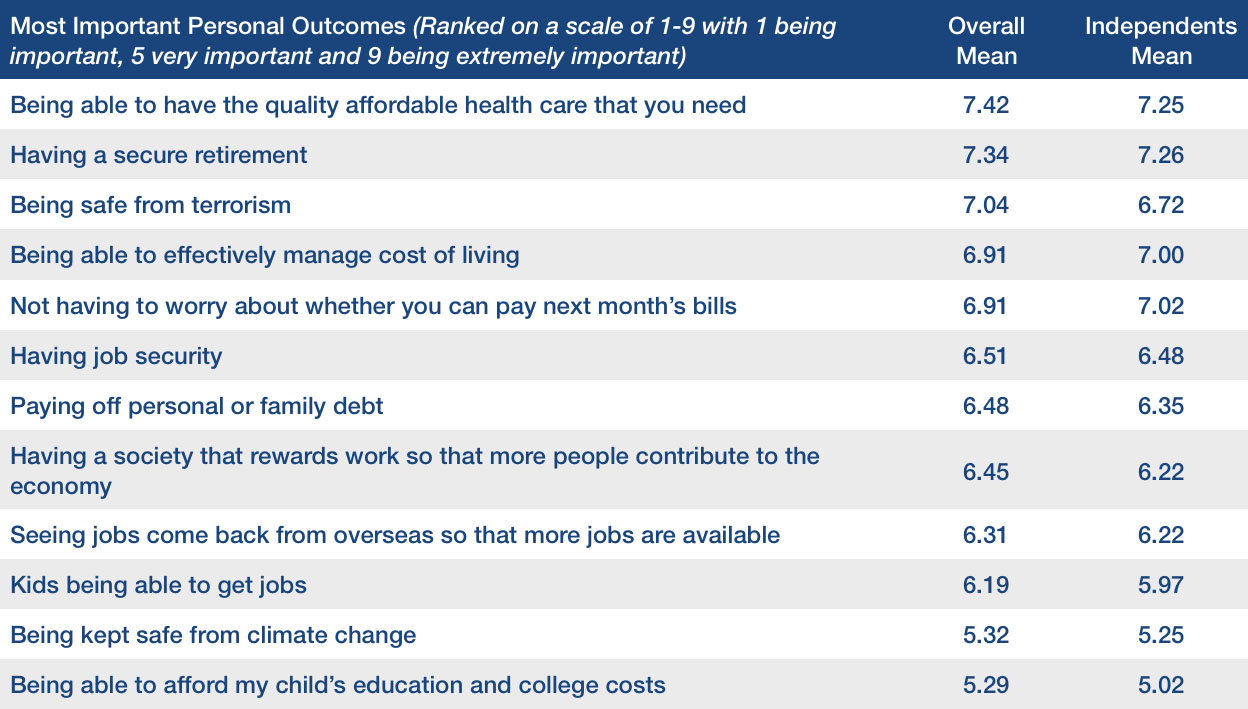

In the survey, we asked a series of personal outcomes and asked voters to rate each one in importance to their lives. Overall, the most important outcomes were being able to have quality affordable health care (7.42) and having a secure retirement (7.34), but with health care being a more prevalent concern among Democrats than independents and Republicans. While there were several important personal outcomes to voter groups, Republicans and independents shared concern about having a secure retirement (7.49 among Republicans, 7.26 among independents), and quality health care (7.47 among Republicans, 7.25 among independents). However in addition to those two outcomes, independents and Democrats also focused on not having to worry about next month’s bills (7.02 among independents and 7.00 among Democrats) and managing cost of living (7.00 among both independents and Democrats). Among Republicans, being safe from terrorism was their top concern (7.58).

Concerns about Retirement

The research indicates that concerns about retirement continue to be very prevalent. Reflecting the priority of “having a secure retirement” as an important personal outcome, one in three voters (30%) says they are in a financial situation that means they will not be able to retire (30-56 yes-no).

Among the group of voters that considers themselves living paycheck to paycheck, over half (53%) say that they will not be able to retire. A quarter (25%) of voters who consider themselves “middle class” also say they are in a financial situation that will not allow them to retire. Regarding confidence in retirement plans including savings and investments, the electorate tends to be only “somewhat confident” (38%), as opposed to “very confident” (18%), “somewhat not confident” (17%) and “not confident at all” (21%).

Economic Outlook

The general economic outlook tends to be somewhat favorable (50-35 right direction-wrong track) but this is largely driven by Republicans who are very optimistic (84-7), more than independents (46-37), with Democrats being negative about the economy (25-57). In terms of a top issue in deciding how to vote for Congress, the economy/jobs emerges as the electorate’s top concern, with 21% indicating it is their most important issue. This is followed by health care/prescription drugs, the top issue for 19% of the electorate.

In terms of how people personally assess whether the economy is working, the clear metric is personal economic issues like income, wages and cost of living (59%), more than macroeconomic figures such as growth rate, inflation or interest rates (18%), the job situation and unemployment rate (11%), and how the stock market is doing (8%). This is an important metric for Republicans promoting the success of the tax plan.

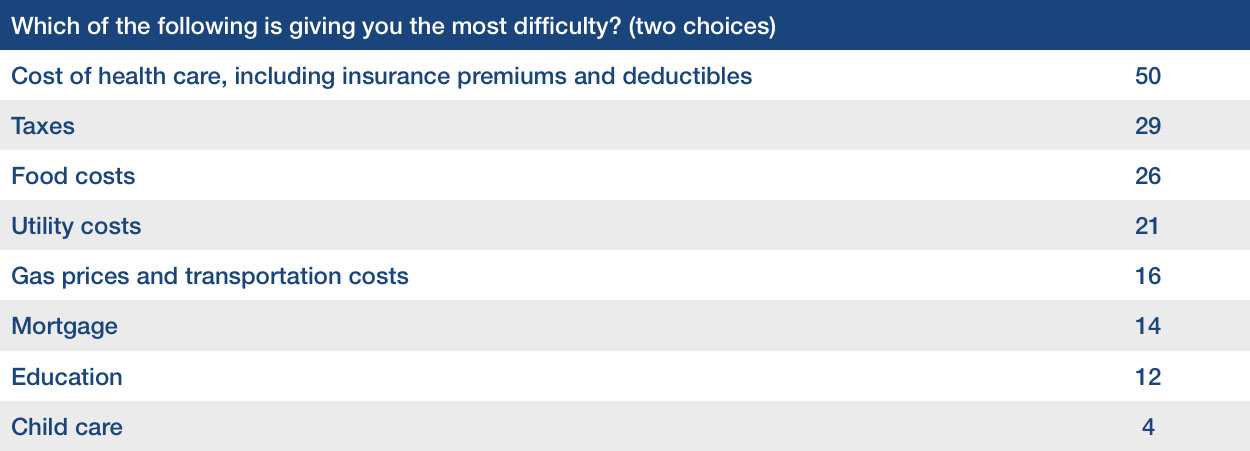

Of cost of living expenses giving people the most difficulty, health care (50%) tops the list, with taxes (29%), food costs (26%) and utility costs (21%) in an important second tier.

The outlook on personal financial situations is favorable (62-22 right direction-wrong track), but as with the general economic outlook, it is Republicans who are very optimistic (83-9) rather than Democrats (49-32). A majority of Independents are also optimistic (55-24), but their optimism does not reach the same level as Republicans’.

Among the 51% of voters who consider themselves to be living paycheck to paycheck, the outlook on their personal financial situation did not reach 50% right direction (47-35 right direction-wrong track). Similarly, 47% of this group believes they will still be in the category of living paycheck to paycheck five years from now (31% believes they will not). Those who consider themselves $400 away from financial crisis, about a third of the electorate (33%) leaned toward saying their personal financial situation was headed in the wrong direction (39-44).

With regard to their family’s financial situation, the plurality of voters have a status quo outlook. Some 46% believe their families’ financial situations will stay about the same, compared to 39% who believe their family’s financial situation will get better in the next year and 11% who think it will get worse. Those living paycheck to paycheck had a similar outlook, with 42% saying their family’s financial situation will stay the same, 38% saying it will get better, and 17% saying it will get worse.

Views about the Tax Bill

One of the opportunities Republicans have to address concerns that voters have is through the recently passed tax bill. Now that the tax bill has been passed, the country is evenly split on supporting the plan (38-39 favor-oppose). However, this is a much better response than when the bill was a Republican plan that had not yet passed. It is still the case, however, that voters remain skeptical that the the tax plan will lower taxes for people like them (36-43 will-will not, with 21% not sure).

Once voters hear some of the basic provisions of the tax reform plan, support increases significantly to 55-27 favor-oppose.

Once they hear some of the basic provisions of the plan, including doubling the standard deduction, reducing overall tax rates, and increasing the child tax credit, support increases significantly to 55-27 favor-oppose. Among Independents, support for the plan improves from 30-37 favor or oppose (with 34% unsure) to 50-26 favor-oppose (with 24% unsure).

Challenges in the Environment

Congressional Republicans continue to struggle with a majority unfavorable brand image (39-56 favorable-unfavorable), but recent passage of the tax bill has helped improve this situation. A Winston Group survey for Winning the Issues at the end of December and prior to the bill’s passage showed Republicans at 35-58 favorable-unfavorable, and a November survey also for Winning the Issues showed the brand at 31-64.

In addition to Republicans, Congressional Democrats continue to struggle with their brand (42-53 favorable-unfavorable). Reflecting the current Congressional generic ballot (-5 R), the country tends to be generally split on who addresses the problems that are important to you (39% Congressional Republicans; 44% Congressional Democrats; 18% undecided).

Brands of the Parties

Respondents were presented with two open-ended questions that asked them what came to mind when they heard the terms “Republicans in Congress” and “Democrats in Congress.” Responses were then grouped with similar responses.

Voters tended to give very general answers, both negative and positive, in response to this question, rather than naming specific issues. Aside from these general negative and positive mentions, voters overall tended to see Congressional Republicans as always fighting and against Democrats, as conservative and for a smaller government, and for the rich. Republicans were even more likely to consider Congressional Republicans as conservative and for a smaller government. Democrats were more likely to consider them to be for the rich, as opposed to the poor or middle class. Interestingly, independents slightly more so than Republicans or Democrats, also named the budget and other economic concerns in relation to Congressional Republicans. Relatively small shares of either party, and an even smaller share of independents, mentioned Trump in their responses.

Voters tended to think of Congressional Democrats as liberal, for big government, or as engaged in wasteful spending. They also generally thought of them as for the people or for the country. Democrats were even more likely to see Congressional Democrats as for the people and country, while Republicans were more likely to see them as liberal and in favor of big government and spending, as well as obstructionists. Independents’ attitudes tended to mimic those of voters overall.

Issue Handling

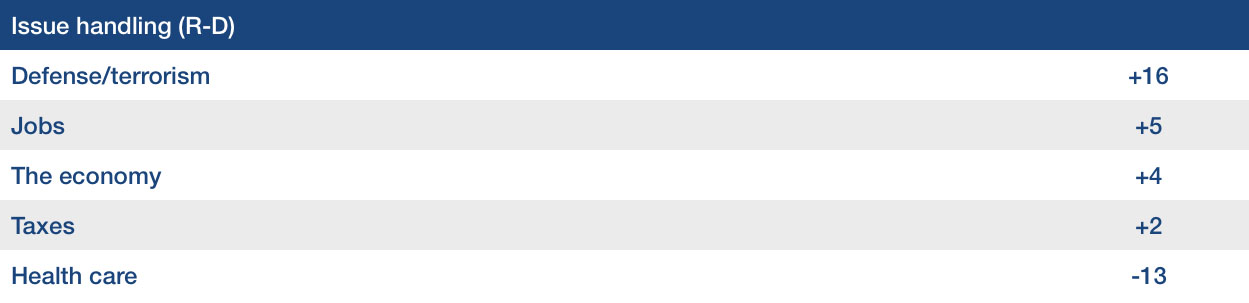

On the issues, the survey shows that Republicans have the clearest advantage on defense/terrorism (+16), followed by smaller leads on jobs (+5), the economy (+4), and taxes (+2). They trail Democrats by 13 on health care.

Presidential Job Approval

President Trump’s overall approval stands at 41-53 approve-disapprove, but his economic job approval (45-43 approve-disapprove) is significantly better. In contrast, his handling of foreign policy (34-54) is lower than his overall approval. Among independents, his overall approval is negative (34-57), but improves on handling of the economy (41-42).

The survey shows that Republicans have the clearest advantage on defense/terrorism (+16), followed by smaller leads on jobs (+5), the economy (+4), and taxes (+2).

In terms of how important a factor is Trump in decisions to vote this fall, the electorate rated him as a moderately important factor: 6.13 on a scale of 1-9, with 1 being not important at all, 5 important, and 9 the most important. He is a more important factor to the two bases (6.41 for Republicans; 6.26 among Democrats) than to the middle (5.68 among independents). He was also a less important factor among Generation Z (5.42).

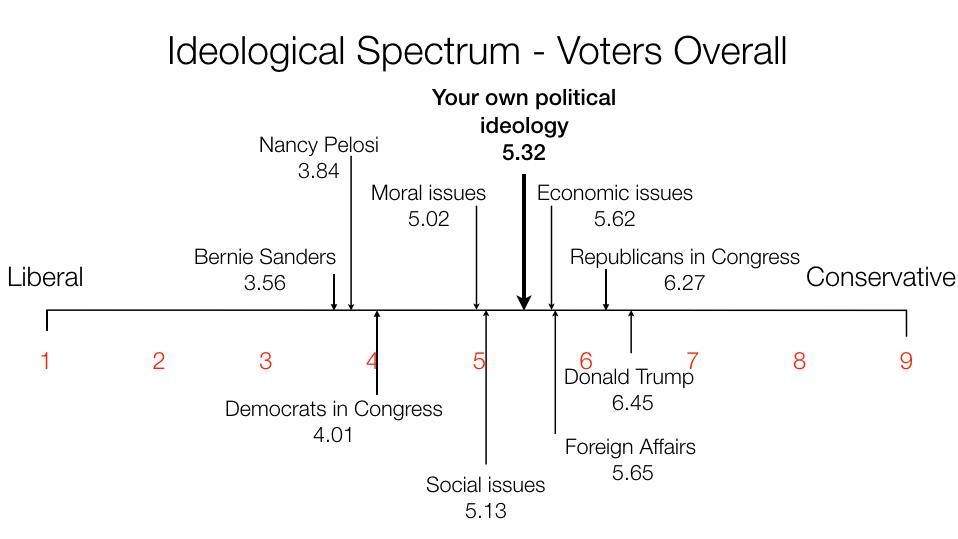

Ideological Outlook

In terms of ideological alignment, the electorate views itself as center-right (5.32 on a scale of 1-9 with 1 being very liberal, 5 moderate, and 9 very conservative). On economic issues (5.62) and foreign affairs (5.65), the country views itself slightly more to the right, but on social issues like education, health care, and the environment (5.13) and moral issues (5.02), the country is even closer to the center than they are with their overall ideology (5.32).

Relative to members of Congress, voters see themselves as slightly closer to the ideology of Republicans in Congress (6.27), than to that of Democrats in Congress (4.01). They saw both Nancy Pelosi (3.84) and Bernie Sanders (3.56) as to the left of their Democratic colleagues in the House and Senate. They saw Donald Trump (6.45) as to the right of themselves and Republicans in Congress.

Voters see themselves as slightly closer to the ideology of Republicans in Congress, than to that of Democrats in Congress.

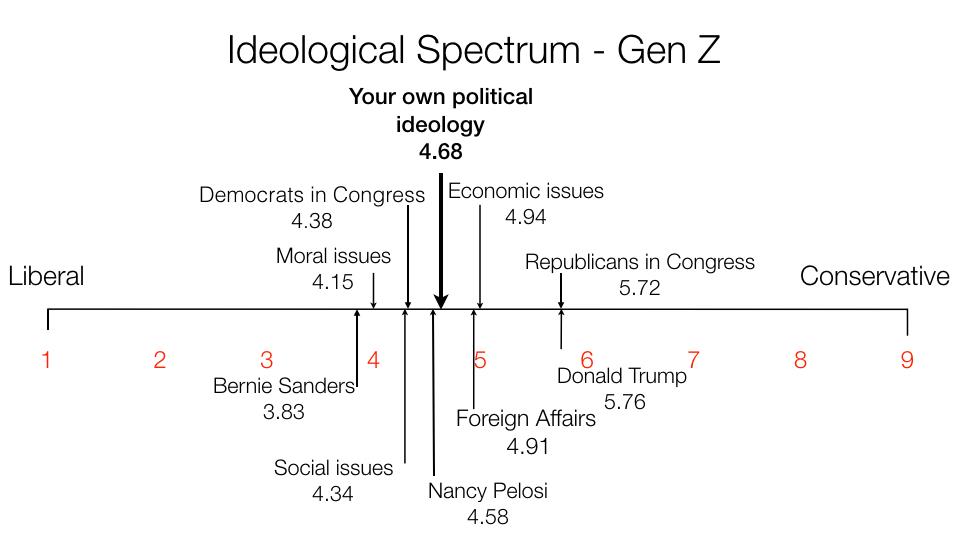

Generation Z voters view themselves slightly left of center (4.68), but describe their ideology on economic issues (4.94) and foreign affairs (4.91) as farther to the right of their overall political outlook. In contrast, they describe their views on moral issues such as abortion and LGBT rights (4.15) and social issues such as education, health care, and environment (4.34) as being slightly to the left of their overall ideology (4.68).

With regard to members of Congress, Generation Z tended to see everything as a little closer to the center. They viewed Congressional Republicans (5.72) as less conservative than voters overall, but still farther to the right of themselves and their ideology on economic issues and foreign affairs than did voters overall. They saw Democrats in Congress (4.38) as less liberal than voters overall, but closer to them in terms of their overall ideology and their ideology on moral, social, economic, and foreign issues. Likewise, they saw Bernie Sanders (3.83) and Nancy Pelosi (4.58) as slightly less liberal than voters overall, and Donald Trump (5.76) as less conservative than voters overall.

Level of Voter Engagement & Likelihood to Vote

In terms of how engaged the electorate is currently, about 1 in 2 voters (47%) describes themselves as more engaged and interested in the political process since the last election, compared to the same (44%) or less (7%). Republican self-described engagement (50%) more interested and engaged) is now on par with the engagement level of Democrats (48%), and higher than that of independents (42%). Liberal Democrats are still slightly more engaged/interested (58%) than conservative Republicans (50%). However, this survey shows that Republicans overall are sustaining their higher level of engagement and interest in the political process, starting to reverse some of the declines we had started to see among Republicans a year ago. A small percentage of the electorate (7%) says they have seriously considered running for public office (7-91 yes-no), but among Generation Z voters, the percentage is higher (12%).

Debating with Friends and Family and Impact of the Media

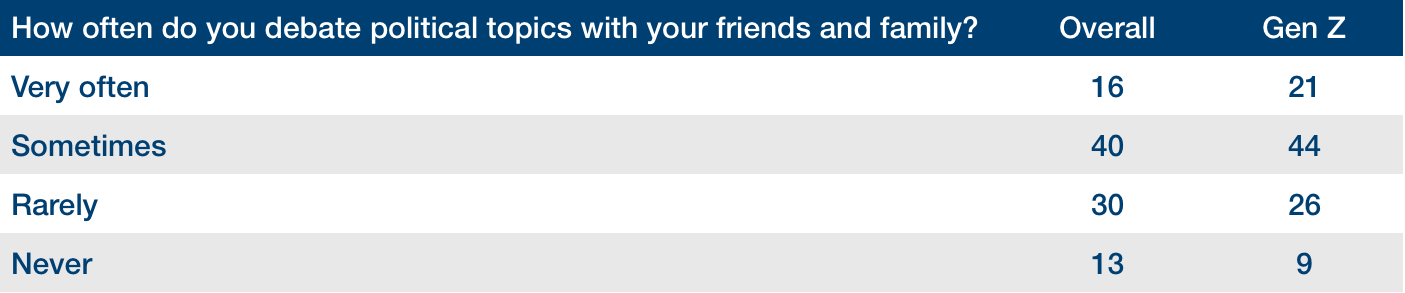

In terms of how often voters debate political topics with friends and family, the largest percentage of the electorate describes the frequency of debate as “sometimes” (40%), rather than “very often” (16%). However among Generation Z voters, the frequency of political debate is higher than voters overall, with 21% describing their debates as “very often” and 44% as “sometimes.”

Generation Z and voters overall agree about the impact of the news media, with 4 in ten voters (40%) and members of Generation Z (40%) saying the media has a “negative impact” in helping them understand national issues and news events.

Influences on Political Views

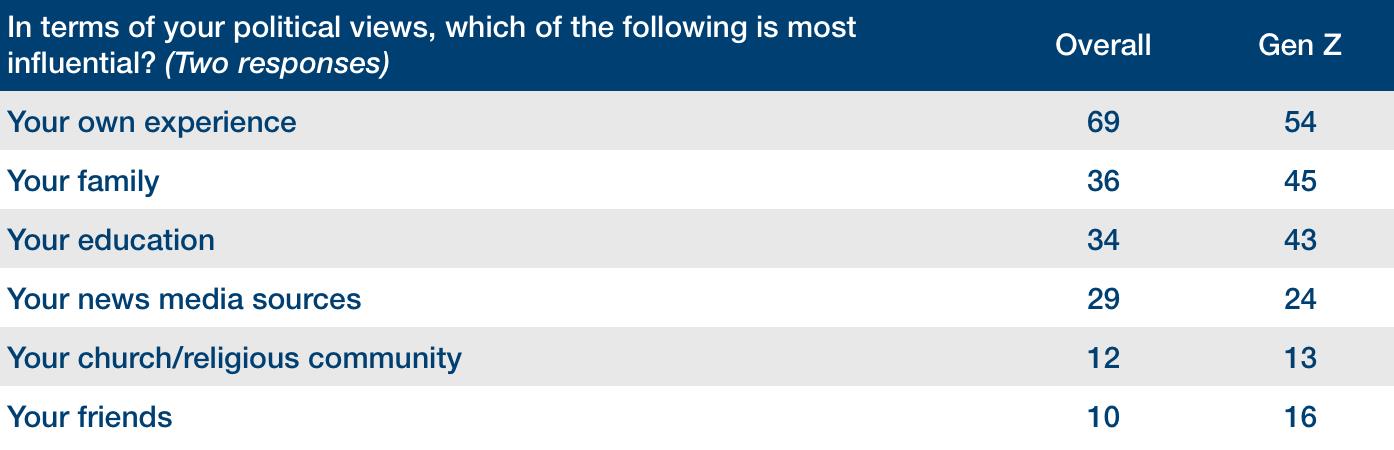

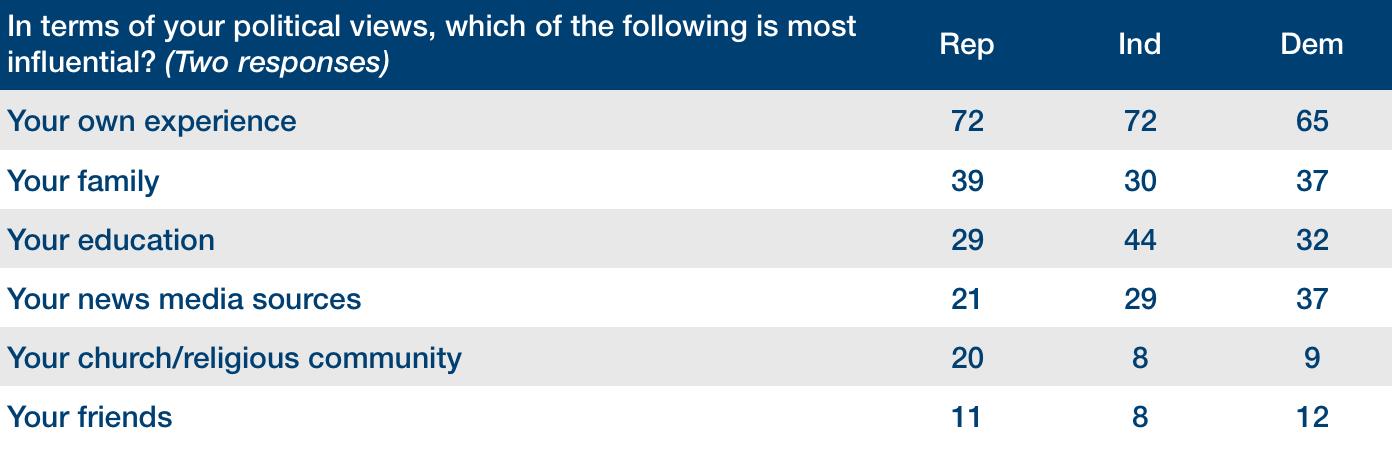

Correspondingly, the news media was not among the most impactful potential influences on a person’s political views, whether a member of Generation Z or not. Both voters overall and Generation Z cited their own experience as the largest influence on their political views. Family and education fell into a second tier of potential influences, followed then by the media. However, Generation Z was more likely to cite family and education and less likely to cite their own experience than voters overall.

There were more differences in how voters form their political opinions, however, by party than there were analyzing Generation Z compared to voters overall. All three parties cited their own personal experience as the most important or second-most important influence on their political views, although somewhat fewer Democrats (65%) said this than Republicans (72%) or independents (72%).

Independents were also the most likely to cite their education as an important influence (44% compared to 29% of Republicans and 32% of Democrats). For their part, Democrats were the most likely to cite their media sources as an important influence compared to independents (29%) or Republicans (21%), but only slightly more than a third (37%) did so. Republicans were twice most likely to cite their church or religious community as an important influence (20%) compared to Independents (8%) or Democrats (9%).

Proposals

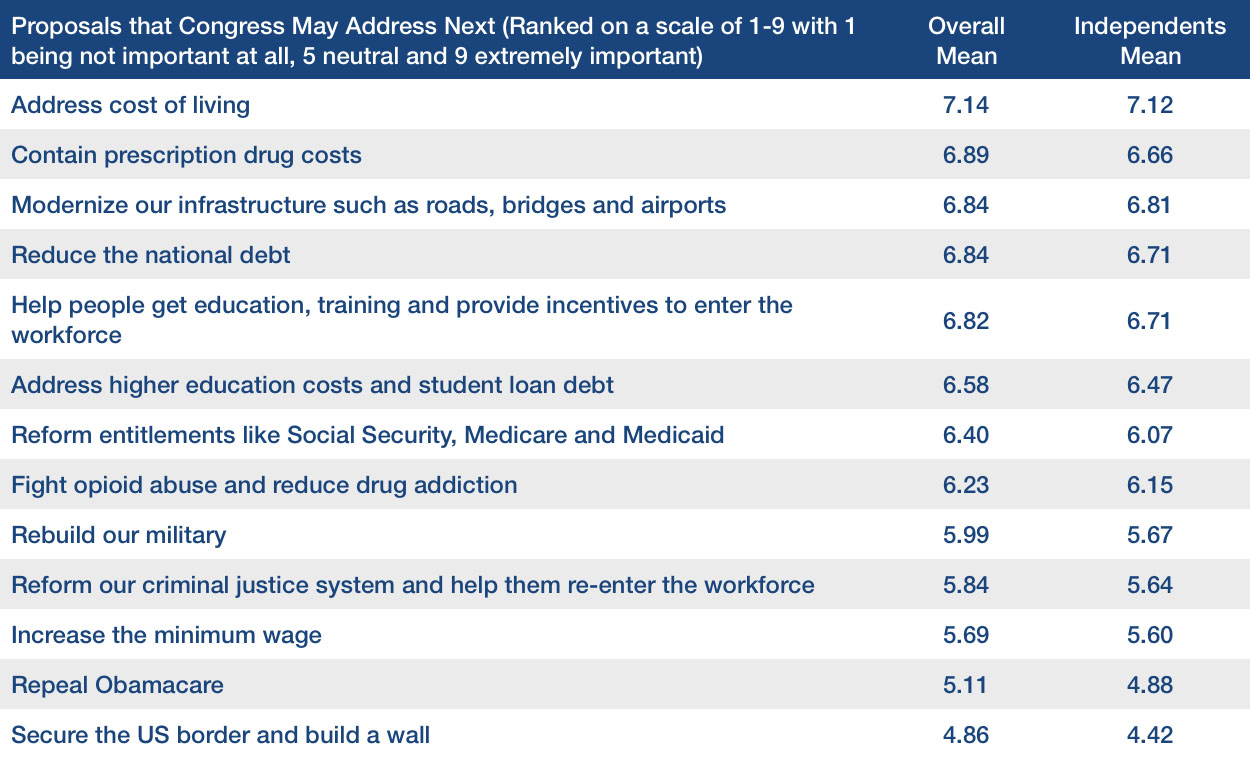

In the survey, we asked voters to rate a series of proposals that Congress may address next. Given the electorate’s concern about financial security, retirement, and cost of living, the proposal that was most important to the electorate was “address cost of living” (7.14), followed by a second tier that included containing prescription drugs costs (6.89), modernizing infrastructure (6.84), reducing the national debt (6.84), and workforce education and training (6.82). It is important to note that the importance of containing prescription drug costs was largely driven by Democratic voters.

Among independents, cost of living was first (7.12), with infrastructure (6.81), workforce training (6.71) and reducing the debt (6.71) being close seconds as priorities. The issues that Congress may pursue next should be evaluated through the lens of helping voters achieve their most important personal outcomes and address problems that voters are facing.

Conclusion

Although the environment remains challenging, Republicans have important opportunities before them as 2018 progresses and the midterms draw closer. Voters are split on supporting the tax plan, but this is an improvement on its standing from when it was a Republican bill that had not yet passed. Support for the plan increases once voters hear some of its basic provisions. By far, voters look to personal economic measures — like wages, income, and cost of living — when assessing how the economy is doing, rather than looking to less personal metrics like unemployment, interest rates, or the stock market. This is an especially salient fact for Republicans looking for ways to promote the success of the tax bill.

Personal outcomes are important, with concerns about cost of living, health care, and retirement at the forefront of voters’ minds. In terms of what issues or proposals that Congress may pursue next, Congress should consider the most important personal outcomes that voters want to achieve, and define and prioritize their proposals in light of how they address the problems that the electorate is facing.

As we pointed out in an article for The Ripon Forum last June, the political outlook for Republicans this fall will largely depend on two basic statistics: how many jobs have been created and whether real wages have increased. The electorate will evaluate whether Republicans have delivered the kind of change, especially economic change, that they as the voters expected. The passage of the tax bill is a step in the right direction, but with the electorate still split on the question about who addresses problems important to them, there is more work to be done to build upon the progress that has been made. Ultimately, the electorate will judge success in terms of their personal economic situations and whether they can see the changes in their own lives.

David Winston is the president of The Winston Group. Myra Miller is the firm’s Senior Vice President and Co-Founder.

_______________________________________

Methodology – This analysis is based on findings from the recent national survey for the Ripon Society of 1000 registered voters and 300 Generation Z voters, defined as those born 1995-1999. The survey was conducted online on January 13-15, 2018.